Multiple Correlation Analysis of Listed SaaS Companies — Market Valuation and Growth Strategies of Japanese and U.S. SaaS Companies

1. Introduction

The average multiple of listed SaaS companies (*EV/revenue (FY1) in this article) has been on a downward trend since the fall of 2021, but as shown in the graph below, it settled at around 5x in the spring of 2022 and has generally remained at the same level since then. This is the same for both in Japan and in the U.S.

However, it is misleading to judge with this number that “the multiples of SaaS stocks are 5x” and it is important to understand the underlying indicators that are influencing the multiples.

In summary, the data shows that for Japanese listed SaaS, as indicators influencing their valuation (multiples) are different, the SaaS stocks in the top 50% ARR and the SaaS stocks in the bottom 50% ARR are two different stories. We believe that SaaS startups’ appropriate strategies vary in the private market, depending on the type of IPO they aim for.

The data in this article is based on about 70 listed SaaS stocks in the BVP Nasdaq Emerging Cloud Comp published by Bessemer Venture partners for the U.S. and about 30 listed SaaS stocks in Japan.

2. Coefficient of determination (R2) for each metric and multiple for U.S. SaaS companies

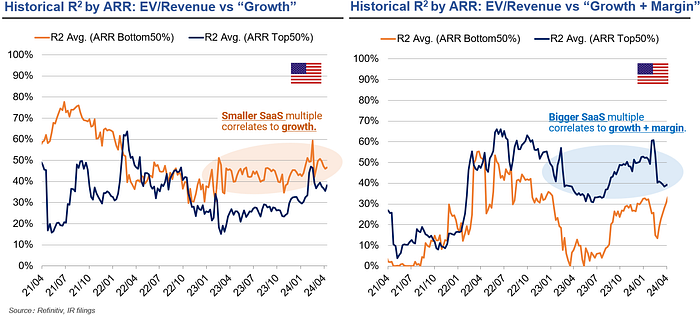

First, to get an overall picture of the U.S. SaaS stocks, please see this graph.

This shows the historical trend of U.S. SaaS stocks in terms of:

- Growth rate and the multiple’s coefficient of determination (R2) (solid orange line)

- Rule of 40 (= growth rate + margin) and the multiple’s coefficient of determination (R2) (solid blue line)

- Growth rate average (dotted orange line)

- Growth rate + margin average (blue dotted line)

From this graph, we can see the general trend for the U.S. SaaS stocks;

- First, in 1Q2022(①), we can see that investors’ interest has shifted to profitability due to the rise in interest rates since the fall of 2021 (the rule of 40 correlation (R2) has risen sharply).

- In 1Q2023 (②), we see the companies shift from growth to profitability (lower growth rate, higher FCF margin) in response to (①).

- In 1Q2024 (③), we see that investors are once again shifting their interest back to growth (growth rate correlation (R2) increases moderately), in response to (②).

In May 2024, during the SaaS session facilitated by DNX at B Dash camp Sapporo, Mr. Kanesaka, CFO of Money Forward (a listed SaaS company in Japan) said, “After 2022, I think there were skeptical thoughts on the part of institutional investors about whether SaaS would really be profitable. However, SaaS companies in the U.S. started to generate solid profits in 2023, and there is a sense that investors are once again returning their attention to growth potential.” The data shows exactly that kind of on-the-ground feeling.

In addition, data from this year show that an indicator weighted by the growth rate, called the “rule of X,” has a stronger correlation with multiples than the traditional rule of 40. It seems that the market as a whole is returning to growth (not growth at all cost as in the past, but an efficient one).

To look at these analyses in a little more detail, we will then look at them by ARR size in the following sections.

3. Coefficient of determination (R2) trends for multiples by ARR size

3–1. Coefficient of determination (R2) of multiples by ARR size for U.S. SaaS

Next, we will see the coefficient of determination (R2) of multiples for SaaS stocks in the U.S., dividing them into the top 50% ARR and the bottom 50% ARR. The boundary between the top 50% ARR and the bottom 50% ARR is approximately $1B.

As you can see, in the U.S., multiples in the bottom 50% of ARR have a strong correlation with growth rate, while multiples in the top 50% of ARR have a strong correlation with growth rate plus profitability.

In other words, in the U.S., it is generally not a good time to be aggressively profitable until the ARR exceeds $1B. Profitability is required from investors once ARR hits a reasonable size.

Now let’s look at SaaS companies in Japan.

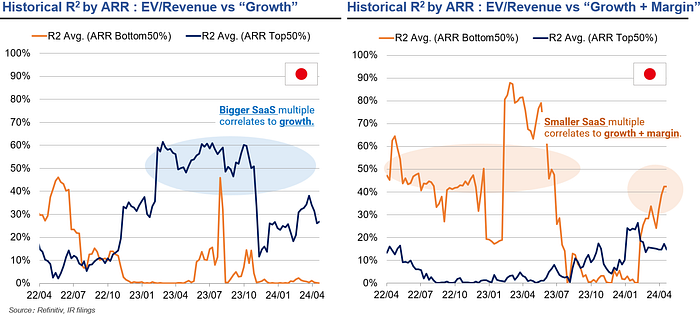

3–2. Coefficient of determination (R2) of multiples by ARR size for SaaS in Japan

Below is the coefficient of determination (R2) of multiples for Japanese SaaS stocks, dividing them into the top 50% ARR and the bottom 50% ARR. Note that the boundary between the top 50% and bottom 50% of ARR is approximately 7 billion yen (Approx. $45M).

In Japan, multiples in the bottom 50% of ARR are strongly correlated with growth plus profitability, while multiples in the top 50% of ARR are strongly correlated with growth.

In summary, the above results indicate that in the U.S.

- SaaS with large ARR: “growth rate + profit margin” influences the multiple

- SaaS with small ARR: “growth rate” influences the multiple

whereas, in Japan,

- SaaS with large ARR: “growth rate” influences the multiple

- SaaS with small ARR: “growth rate + profit margin” influences the multiple

The result is exactly opposite between Japan and the U.S.

3–3. Are Japanese SaaS multiples in the bottom 50% ARR really correlated with the rule of 40?

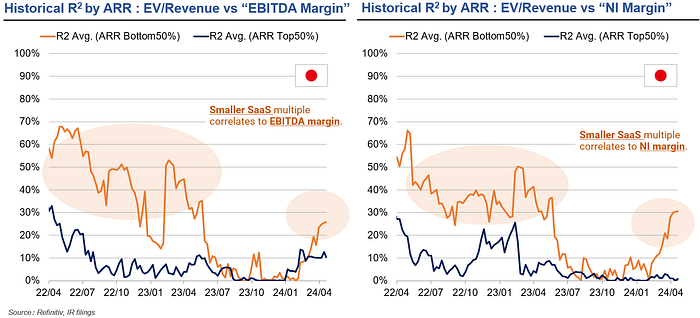

While the above results show that multiples for Japanese SaaS with small ARR size have a strong correlation with “Growth Rate + Profit Margin,” let’s look at this in more detail.

For example, the following graph shows the coefficient of determination (R2) between multiples and EBITDA margin and Net Income margin for the top 50% and bottom 50% of ARR. As you can see from this graph, the multiples of Japanese SaaS with smaller ARR size have a stronger correlation with these margin indicators.

In combination with the weak correlation with growth rate, it seems reasonable to interpret that Japanese SaaS stocks with small ARR are evaluated not by SaaS indicators such as rule of 40 or ARR growth rate, but by general profit indicators.

This may be due to the difference in investor composition. In other words, SaaS stocks with smaller ARR sizes in Japan have more retail individual shareholders (who are not necessarily familiar with tech stock valuations), so it does not really matter whether they are SaaS companies or not. They are evaluated based on uniform criteria with stocks in other industries and sectors, such as PER. On the other hand, when it comes to SaaS with a large ARR, overseas institutional investors who are familiar with evaluating tech stocks come in, and it seems that they are evaluated based on top-line growth potential.

4. Distribution of Japanese SaaS Companies (Sales & Sales Growth)

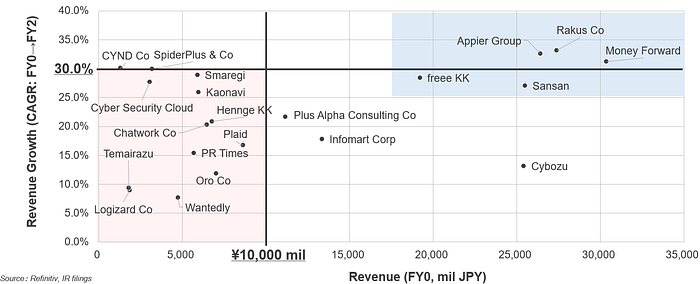

Now, I would like to look at this point from a slightly different perspective. The following graph plots Japanese SaaS stocks with recent revenues on the horizontal axis and growth rate (CAGR: FY0→FY2) on the vertical axis (※limited to stocks for which sales forecast for the next fiscal year (FY2) is available).

As shown in the graph, Japanese SaaS can be roughly divided into two zones: the red zone (revenues of less than 10 billion yen(approx. $64M) and annual growth rate of less than 30%) and the blue zone (revenues of 10 billion yen(approx. $64M) or more and annual growth rate of about 30% or more). We can see that for domestic SaaS, companies with large revenues also have high growth rate.

We also interviewed several major investment banks and learned that large SaaS stocks in the blue zone (sales of 10 billion yen(approx. $64M) or more and annual growth rate of 30% or more) are generally evaluated by EV/Revenue, while small- and medium-sized SaaS stocks in the red zone are basically evaluated mainly by PER and other profit factors.

As for the small- and mid-cap listed SaaS stocks in the red zone,

- There are skeptical thoughts on growth potential due to the small TAM, difficulty in drawing growth strategies, and concerns that they may not be able to differentiate themselves and to create sufficient moat. Therefore, there is a relative need to generate profits (if there is limited room for growth)

- It is difficult for foreign institutional investors, who are price leaders in the Japanese stock market, to get into the market, and retail investors end up to take a relatively large part. Retail investors tend to look at general profit indicators rather than ARR growth rate or rule of 40, which are often seen in SaaS.

- Small and mid-cap stocks have difficulty in raising large amounts of capital for growth after going public, and management is forced to make profits. As a result, the growth rate is compromised.

The combination of various factors like above makes it a different game than SaaS stocks in the blue zone.

In the context of the private market, — the ARR growth rate generally diminishes with the ARR size, so a SaaS startup with an ARR of less than ¥3 billion($19M) and a growth rate of less than 30%, for example, is unlikely to be valued aggressively at EV/ Revenue at the time of IPO, like a company in the blue zone in the upper right of the table, and therefore they will have a hard time to raise funds from VC at a high valuation.

5. Liquidity

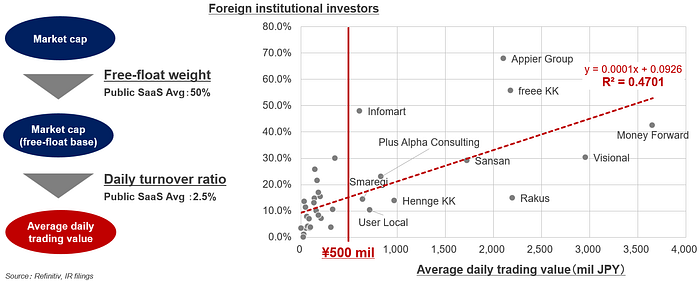

I mentioned above that small-cap stocks are difficult for foreign institutional investors to enter, but I would like to look at this point from the perspective of liquidity.

First of all, according to interviews with several investment banks, it is foreign institutional investors that support the valuations of Japanese tech stocks from a fundamental perspective, and thus it’s important to create sufficient liquidity in order to attract these foreign institutional investors as shareholders. What is the standard for liquidity? In order to attract overseas institutional investors who can become price leaders, liquidity of 500 million yen(approx. $3.2M) or more in average daily trading value is standard. In fact, the following chart plots Japanese public SaaS stocks in terms of the ratio of foreign corporate/institutional shareholders and average daily trading value, and the results are generally consistent.

Next, let’s back-calculate the market cap to achieve ¥500 million in average daily trading value. A rough average of the daily turnover ratio of floating shares is about 2.5%, and the free-float weight is roughly 40–50%. This means that to secure daily trading value of ¥500 million, a market cap of ¥40–50 billion(approx.$260–320M) is required.(¥500 million(approx.$3.2M) ÷ 2.5% ÷ 40–50%)

In other words, to attract foreign institutional investors who will be price leaders at the time of the IPO, an estimated market cap of 40–50 billion yen(approx.$260–320M) is required.

Of course, even with a lower estimated market cap (e.g., 20–30 billion yen (approx.$160–190M)), it is possible to secure a daily trading value of 500 million yen(approx. $3.2M) by raising the offering ratio at the time of IPO to increase the free float weight. However, there are various issues to be considered, such as whether investor demand will be enough to handle the offering and whether existing shareholders will respond to the offering at the time of the IPO. The composition of middle- and late-stage investors is an important issue for CFOs of tech startups aiming for an IPO, from the perspective of creating liquidity after the IPO.

6. Summary

I would like to briefly summarize the findings so far.

SaaS stocks’ multiples in the U.S.,

- SaaS with large ARR: “growth rate + profitability” influences the multiple

- SaaS with small ARR: “growth rate” influences the multiple

whereas in Japan,

- SaaS with large ARR: “growth rate” influences the multiple

- SaaS with small ARR: “general profit index” influences the multiple

We have explained that domestic SaaS stock can be divided based on “10 billion yen revenue and annual growth rate 30%,” and SaaS stocks with a revenue of less than 10 billion yen(approx. $64M) and an annual growth rate of less than 30% are likely to be evaluated based on general profit indices. We also mentioned that in order to attract overseas institutional investors who can become price leaders, liquidity of 500 million yen(approx. $3.2M) or more in terms of average daily trading value and an estimated market cap of 40–50 billion yen(approx.$260–320M) are the guidelines.

7. Closing

Japan Exchange Group discloses the following data on the current status of the Growth Market.

ー Market cap level of the Growth Market;

- The median market cap of companies listed on the Growth Market is 6 billion yen(approx.$38M)

- 31% of companies have not met the current requirement of 4 billion yen(approx.$26M)

ー Post-IPO growth of the listed companies in the Growth Market;

- The median market cap growth is 1.03x since IPO

- 49% of companies market caps are below the market capitalization at the time of IPO

- Even when looking at growth by the number of years since IPO, there are only a limited number of stocks that have grown significantly above their market cap at IPO

The above data is for the whole growth market, but it illustrates how difficult it is to grow after a small-cap IPO. In particular, in the SaaS business model, which requires upfront investment and is mainly based on subscription-based revenues, it should be more difficult to achieve significant growth after a small-cap IPO, being required to generate profits in the short term as public companies and facing difficulty in raising funds for growth in a flexible manner once the company is listed in small cap. MoneyForward’s CFO Mr. Kanesaka commented, “In the current SaaS environment, SaaS startups should take their time in the private market rather than rushing to IPO.” We think that if a SaaS startup is aiming for a large-cap IPO, it should raise a large amount of capital in the private market and stay private to invest upfront until the ARR reaches a reasonable size over time.

Conversely, if a SaaS company is looking at a small/mid cap IPO with an ARR below 5 billion yen, it is necessary to start preparations several years before the IPO in order to build a business model that can generate a profit. In this case, if a company raises cash based on revenue multiples in the private market, a distortion in the evaluation method will occur as they will be evaluated based on profit indicators at the time of IPO, so the finance strategy, especially for mid/later-stage SaaS startups, should be carefully considered.

Which option to choose ultimately depends largely on the outlook of TAM and growth strategy, including multi-product, target expansion, global expansion, and M&A. Especially for SaaS startups around Series B, it is necessary to steer IPO strategy in accordance with growth strategy and its prospects while also taking public market trends into consideration.

(Shuhei Nitta / Investment VP, DNX Ventures Japan)